Two Truths and the 20B Lie : Duolingo is Wildly Overpriced

A brilliant company—but the $20B price tag doesn’t add up.

“How can we get 100 million people to translate the web into every major language—for free?” That’s the question Duolingo’s founder and current CEO Luis von Ahn asked his grad student, Severin Hacker. In one of the most engaging TED Talks out there, Luis laid out his original vision for Duolingo. The idea was simple: teach people a new language, then have them use it to translate the web, line by line. He wasn’t new to crowdsourcing. With the earlier projects, CAPTCHA and reCAPTCHA, Luis had already turned online communities into tools for digitizing books—using the collective strength of communities to translate books one word at a time.

It’s been almost 15 years since that talk aired, and Duolingo has come a long way. Today, it’s the go-to platform for anyone looking to learn a new language. Their green owl mascot —Duo— is everywhere, and the brand shows up in countless memes, parodies, and jokes—almost always in a good-humored way.

For the past seven years, I’ve used Duolingo daily to learn Spanish. It’s addictive, to say the least. I usually spend 5 to 10 minutes a day doing lessons, hi-fiving other learners and collecting points for a spot on the weekly leaderboard. My daily streak is what keeps me going. If you ask how good my Spanish is after all this time? I’d say, “No bueno.” I can read signs and understand restaurant menus, but I can’t hold a real conversation or read long sentences. Most of what I say is broken and badly mispronounced. But that’s okay. I never planned to master the language. I started using the Duolingo app for fun and now it’s a habit I can’t break. My streak gives me bragging rights—especially when I need a solid “truth” for two truths and a lie.

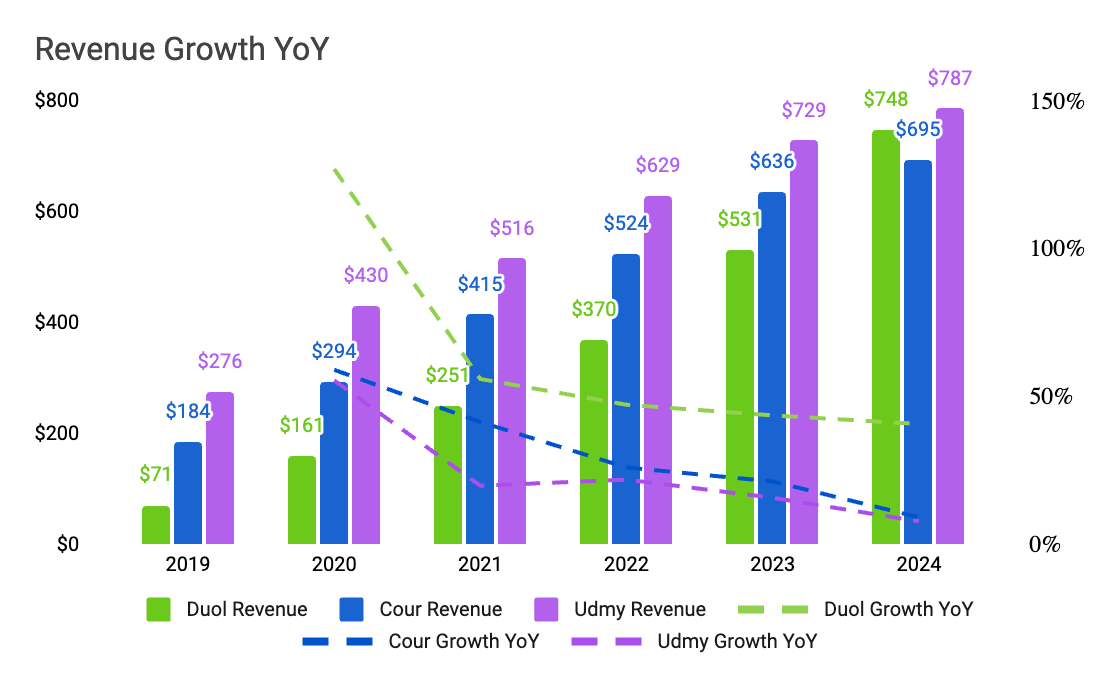

Given Duolingo’s popularity, it’s no surprise the company is doing well financially. Its revenue has grown from $250 million in 2021 to almost $800 million in just three years. As a public company, its stock has soared over the last year - from a modest $160 per share to over $500 in recent months.

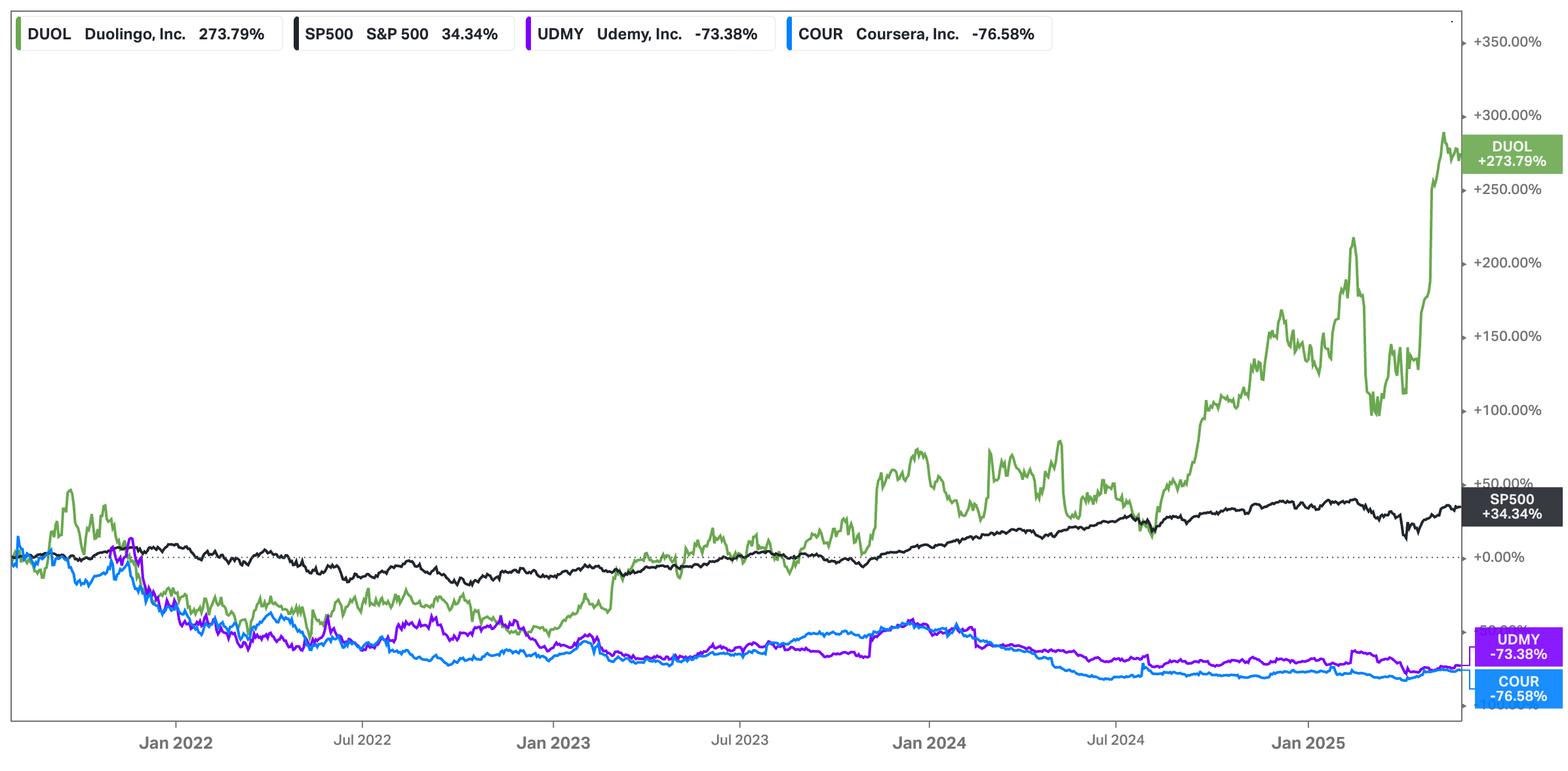

For a quick comparison, a dollar invested in Duolingo at IPO would now be worth $3.73. That same dollar in the S&P 500 would be worth $1.34, while a dollar in either Coursera or Udemy would have shrunk to just 25 cents.

Given the stock’s sharp run-up, I wanted to dig deeper: Has something fundamentally changed about the business—or is this just unbridled market exuberance?

Business Model

For those unfamiliar with how Duolingo makes money: it’s a language learning app that teaches 40+ languages and has recently expanded into Music, Math, and Chess. The company runs on a “freemium” model—anyone can sign up and start learning for free. For those who want all the bells and whistles, Duolingo offers paid subscriptions ranging from about $120 to $240 per year for its top-tier “Max” plan. For comparison, Netflix’s highest plan costs around $300 annually, and Coursera’s subscription runs about $400.

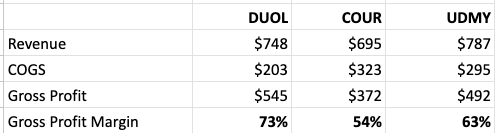

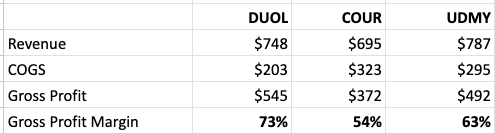

In 2024, Duolingo generated ~ $750M in revenue with a gross profit of 73%. It earns revenue from three primary sources:

Subscriptions and In-App Purchases - This is the core of the business, accounting for over 85% of total revenue. Year over year, this segment has grown at a healthy 50% clip.

Advertising - Duolingo has a massive user base of around 100M active users and has found a way to monetize it. About 8–10% of this user base turn into paying subscribers to get the ad-free, souped-up learning experience. The remaining 90% see ads, usually at the end of lessons. Advertising contributes roughly 7% of total revenue and has historically grown at around 10% annually.

Based on my personal experience, I expect this segment to grow faster and play a larger role in the revenue mix. Duolingo appears to be tweaking the free user experience to increase ad engagement. To its credit, the ad experience still doesn’t feel intrusive or over-the-top. Ads are only shown after lessons, and there are no pop-ups or interstitials to battle through—everything remains thoughfully integrated.

Language Proficiency Tests - Duolingo has developed its own English proficiency exam called the Duolingo English Test (DET). These tests are typically required by universities as a part of the admissions process for international applicants. Duolingo competes with well-established players like TOEFL and IELTS in this space.

A DET typically costs around $70, while a TOEFL exam can run up to $300 depending on location. While the DET is clearly more affordable—and Duolingo is positioning itself as a disruptor in the space—it’s still accepted by far fewer institutions: about 5,500 compared to over 13,000 for TOEFL. This segment contributes roughly 6% of Duolingo’s total revenue and is growing at a modest 10% annually.

Duolingo vs Coursera vs Udemy

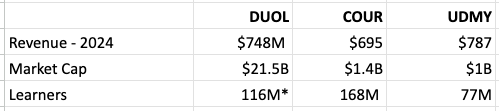

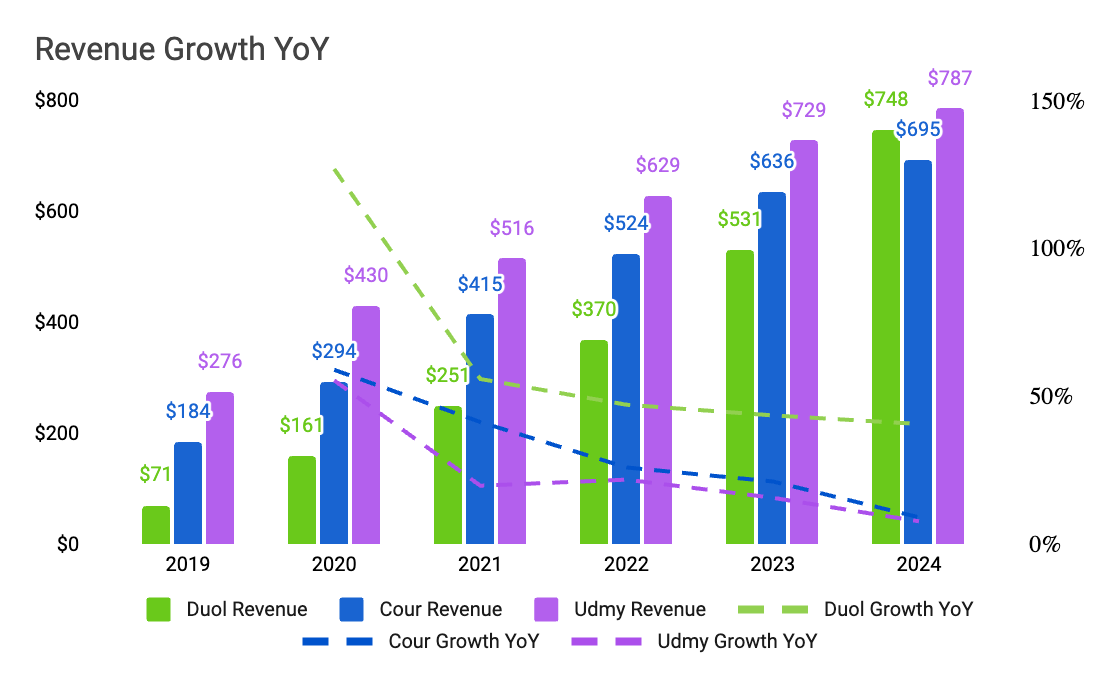

Duolingo, Udemy and Coursera are ed-tech that have been around for over a decade, all three companies went public in 2021, they each have millions of learners and they generate annual revenues of roughly 700M to 800M. In spite of their similarities, as public companies their fates have been starkly different. Today Duolingo is valued at over $20B while Coursera and Udemy hover around the billion dollar mark

Why do these companies have such diverging valuations? It boils down to three simple reasons - margins(driven by content and acquisition costs), growth rates and pricing power.

Margins

Content Ownership Costs: In the case of Duolingo, all the learning content within the app is owned by the company - they don’t have to pay hefty fees to third-parties for creating their content. This gives Duolingo solid gross margins of 73%.

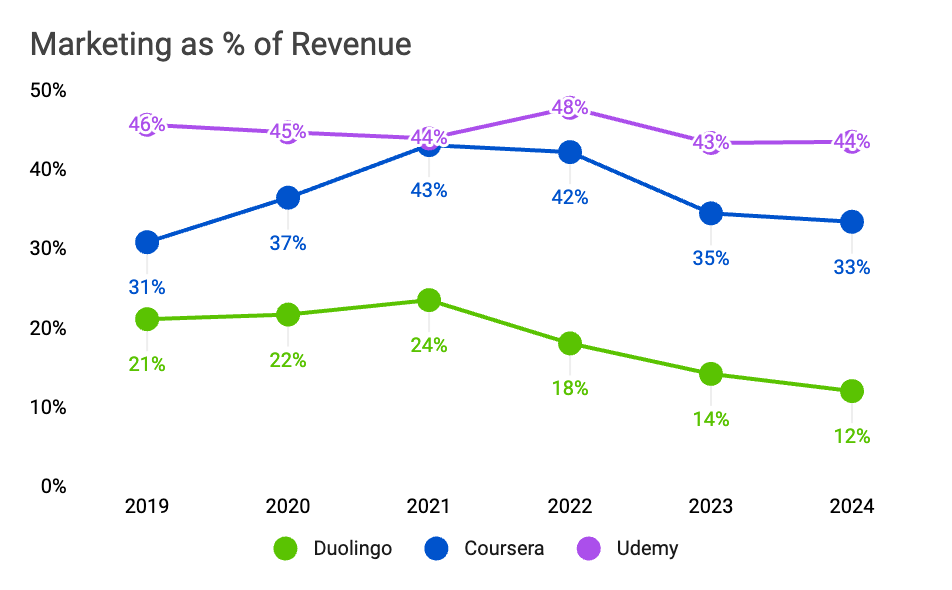

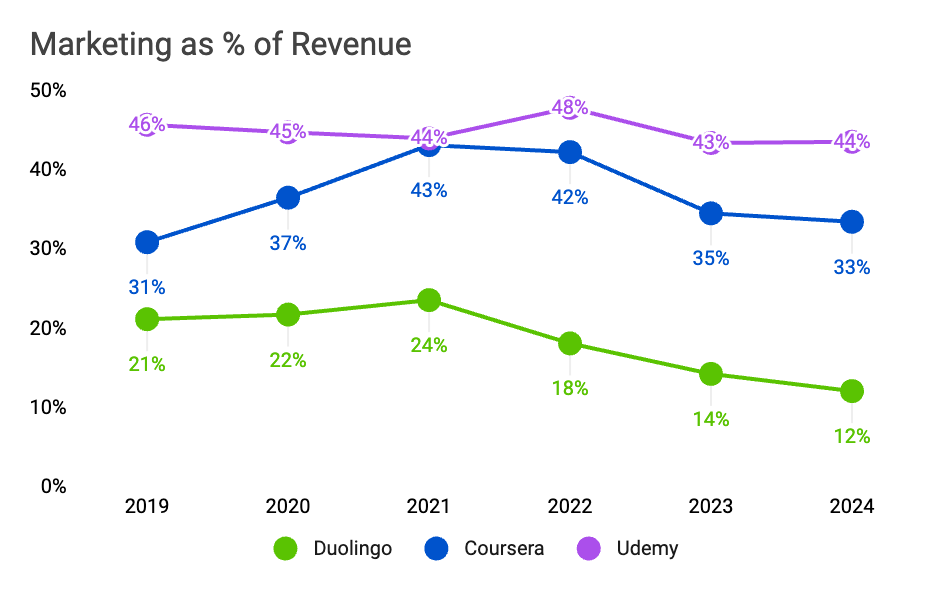

Acquisition Costs: Being a part of pop culture, internet memes and late night comedy shows comes with benefits. Free publicity equates to lower marketing expense. While Coursera and Udemy have to spend nearly 30 to 40% of their revenue to prop up growth, Duolingo spent a little over 10% in 2024. From the chart above is also easy to see that as a percentage of overall revenue their marketing costs for Duolingo, have been declining every single year.

Growth Rates

In 2024, Duolingo leapfrogged Coursera’s annual revenue and is on track to surpass Udemy’s as well. Its revenue has been growing at over 40% annually, driven in part by its ability to convert its large base of 100 million free users into paying customers at a much faster rate than either Coursera or Udemy. Around 8% to 10% of Duolingo’s users become subscribers each year—compared to an estimated 2% for either Udemy or Coursera.

Pricing Power

Unlike Coursera and Udemy, which frequently rely on steep discounts to drive sign-ups, Duolingo rarely runs promotions. I’ve only seen one—and it’s a limited offer they roll out during the last week of December, aimed at users making New Year’s resolutions. Outside of that, the promotional playbook has been notably quiet.

Moreover in 2023, Duolingo introduced a more expensive pricing plan aptly called Max. The Max plan is almost twice as expensive as its next lowest tier. While the company hasn’t disclosed how many users have adopted it, the move signals a clear push to increase monetization and test the upper limits of its pricing power.

Intrinsic Valuation

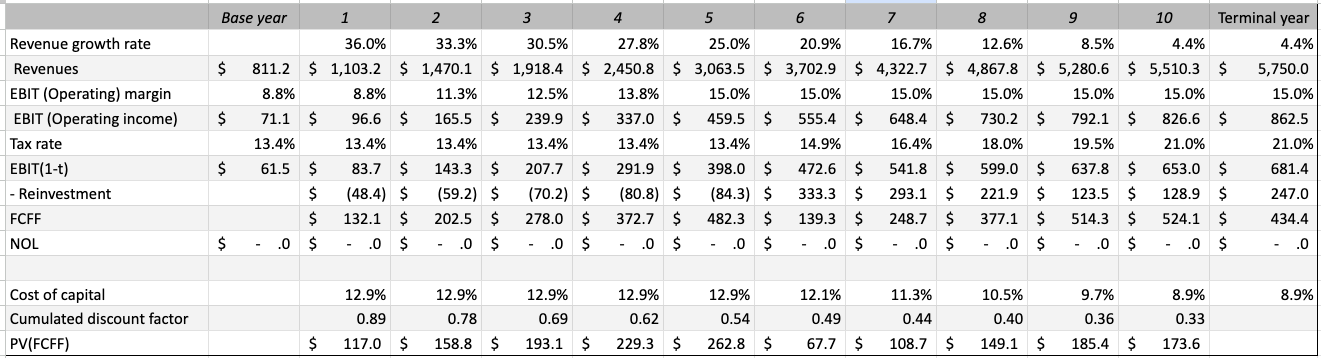

It’s time for some number crunching. Since the value of a stock is the present value of its expected future cash flows, we have to project Duolingo’s earnings and margins

Revenue Growth: Although Duolingo’s revenue has been growing over 40%, year over year the growth rate has been declining. This is expected, based on basic arithmetic—each year, you're working off a larger base. I’ve assumed revenue will grow 36% in 2025 and drop to 25% by year 5. By year 10, growth will decline to the risk-free rate of 4.35%.

Margins: Their current pre-tax operating margin is 8.76%. I’m assuming that this will improve to 15% over the next five years as they continue iterating tweaking the product. Additional monetization opportunities—product promotions, more ad impressions, etc.—could boost margins further.

Historically, app-based businesses have had to pay hefty fees — close to 30% to app stores owned by Google and Apple. This is currently being challenged in court and could lead to either lower fees or the freedom to bypass the app store checkouts altogether. That shift alone could meaningfully impact margins.

Outstanding Shares: Duolingo has 39.2M Class A shares, 6.2M Class B shares, and 1.6M RSUs outstanding. They also have 1.8M performance-based RSUs reserved for founders, tied to stock price hurdles. I’m assuming 65% of these performance based RSUs (i.e. 1.2M) will vest. Total shares outstanding: 39.2M + 6.2M + 1.6M + 1.2M = 48.27M.

Lastly, Duolingo has roughly 1.2M options outstanding. I’ve valued those options using Black-Scholes at about $568M.

Taking the present value of its future cash flows and terminal value, adding cash and subtracting the value of options gives me a value of equity of $5.27B. Dividing the value of equity by the number of outstanding shares of 48.27M leads me a share price of roughly $110/share. The stock is currently trading at $472/share at over a 400% premium over its intrinsic value.

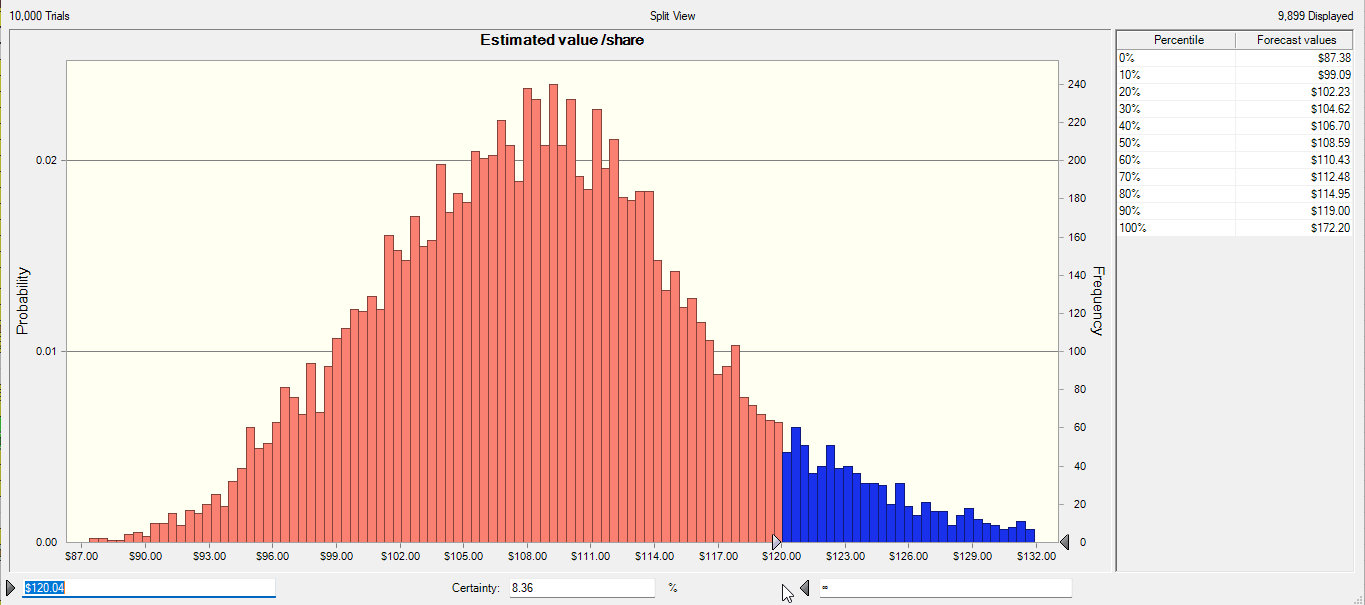

Factoring in Uncertainty

To factor in uncertainty I varied a few inputs -

Revenue growth between 20% and 30% over the next five years

Margins between 12% and 20% (lognormal distribution)

A negative correlation between growth and margins, since cutting marketing expense (to boost margins) could slow down user growth.

After running 10,000 simulations my model indicates that there is barely 10% chance that the value of Duolingo is above $120/share.

Bottomline

Summing it all up, I’m genuinely impressed by what Duolingo has achieved in the ed-tech space. They’ve made learning fun, engaging, and accessible—and in many ways, have stayed true to their original vision. If it weren’t for Duolingo, I doubt I would’ve picked up another language (even the little I know), and I’m sure there are millions of learners like me—people using the app not to become fluent, but as a low-effort way to build a new skill.

As a company, Duolingo presents a compelling growth story. Its healthy margins stem from a strong operating model and disciplined approach to marketing. “Mutually reinforcing flywheel” is what they like to call it: a large learner base, low-cost word-of-mouth driven growth, which leaves more room to invest in product quality, which then converts more paying users—and improves margins further.

More recently, their CEO jumped a bit too hard on the AI bandwagon — with a company letter and all. After some very predictable backlash, he dialed down the rhetoric. Tone-deaf missives aside, the intent is clear: Duolingo seems increasingly willing to let pedagogy take a backseat in pursuit of profits.

I’m skeptical about the long-term sustainability of Duolingo’s model. Freemium platforms grow by casting a wide net and then slowly increasing friction to convert the free base into paying customers—but there’s only so much that can be taken away before users start to leave amass. Duolingo may be nearing that threshold. Reddit forums are filled with users criticizing recent changes that make the free experience more restrictive.

In the end, here are the hard truths: Duolingo is a fantastic ed-tech company, and the brand they’ve built is remarkable. But as an investor, given that the stock is trading at nearly 4x my intrinsic estimate, I’ll give it a hard pass.

Disclaimer: This analysis is for informational purposes only and does not constitute investment advice, a recommendation, or an offer to buy or sell any securities. Please conduct your own research or consult a financial advisor before making any investment decisions.

Thank you. I just opened my position on Duolingo after the recent fall since valuation seems fairly priced. I see Duolingo as a "fun" learning app. There are better ways out there to learn languages, but Duolingo makes it casual and funand they really don't have much competition in that space. Someone serious about learning always have better ways out there but Duolingo is about making it casual

Great article, crazy seeing what is happening to DUOL today.